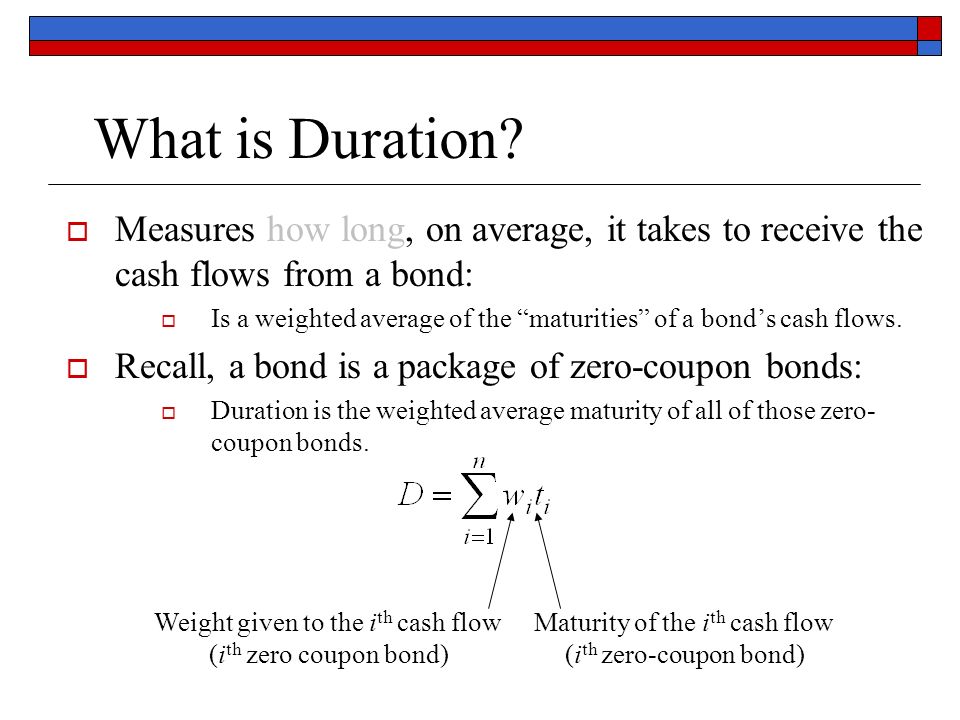

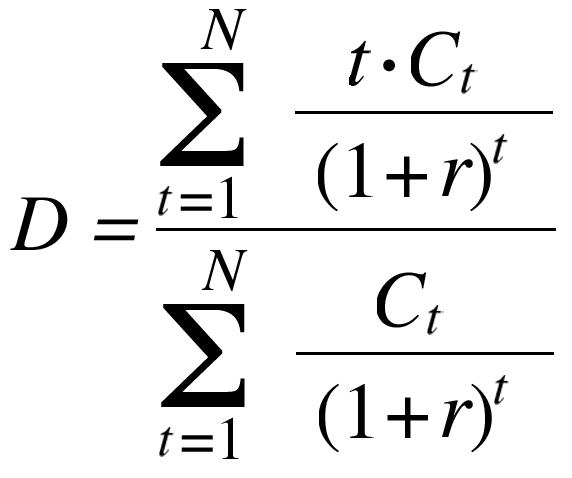

43 duration for zero coupon bond

monevator.com › bond-durationBond duration: how it works and how you can use it - Monevator Oct 25, 2022 · What is bond duration? Bond duration expresses a bond’s vulnerability to interest rate risk. The larger the bond duration number, the more reactive a bond’s price is to interest rate changes, as the bond’s yield adjusts to reflect those changes. For example, if a bond’s duration number is 11, then it: › terms › dDuration Definition and Its Use in Fixed Income Investing Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ...

dqydj.com › zero-coupon-bond-calculatorZero Coupon Bond Calculator – What is the Market Price? - DQYDJ P: The par or face value of the zero coupon bond; r: The interest rate of the bond; t: The time to maturity of the bond; Zero Coupon Bond Pricing Example. Let's walk through an example zero coupon bond pricing calculation for the default inputs in the tool. Face value: $1000; Interest Rate: 10%; Time to Maturity: 10 Years, 0 Months ...

Duration for zero coupon bond

› articles › bondsUnderstanding Bond Prices and Yields - Investopedia Jun 28, 2007 · A bond's coupon rate is the periodic distribution the holder receives. ... How to Calculate Yield to Maturity of a Zero-Coupon Bond. ... Duration indicates the years it takes to receive a bond’s ... Ομόλογο - Βικιπαίδεια Ομόλογο μηδενικού επιτοκίου (Zero coupon bond). Ομόλογα που δεν προβλέπουν ενδιάμεσες πληρωμές κουπονιών. Συνήθως έχουν διάρκεια από 1 έως 3 χρόνια. Υπάρχει μια αρχική πληρωμή από τον αγοραστή προς ... › ask › answersThe Macaulay Duration of a Zero-Coupon Bond in Excel Aug 29, 2022 · The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount.

Duration for zero coupon bond. › zero-coupon-bondZero Coupon Bond - (Definition, Formula, Examples, Calculations) = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest Compound Interest Compound interest is the interest charged on the sum of the principal amount and the total interest amassed on it so far. › understanding_durationUnderstanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds’ durations, you may be able to anticipate the degree of › ask › answersThe Macaulay Duration of a Zero-Coupon Bond in Excel Aug 29, 2022 · The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount. Ομόλογο - Βικιπαίδεια Ομόλογο μηδενικού επιτοκίου (Zero coupon bond). Ομόλογα που δεν προβλέπουν ενδιάμεσες πληρωμές κουπονιών. Συνήθως έχουν διάρκεια από 1 έως 3 χρόνια. Υπάρχει μια αρχική πληρωμή από τον αγοραστή προς ...

› articles › bondsUnderstanding Bond Prices and Yields - Investopedia Jun 28, 2007 · A bond's coupon rate is the periodic distribution the holder receives. ... How to Calculate Yield to Maturity of a Zero-Coupon Bond. ... Duration indicates the years it takes to receive a bond’s ...

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

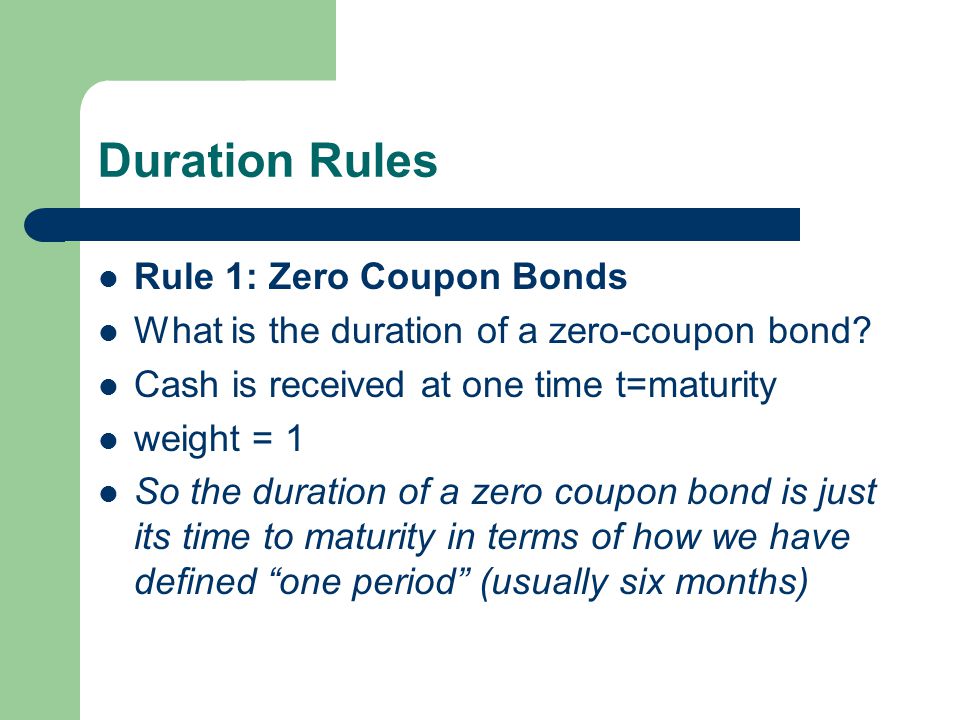

Interest-Rate Risk II. Duration Rules Rule 1: Zero Coupon ...

Price of a defaultable zero coupon bond price in each time t ...

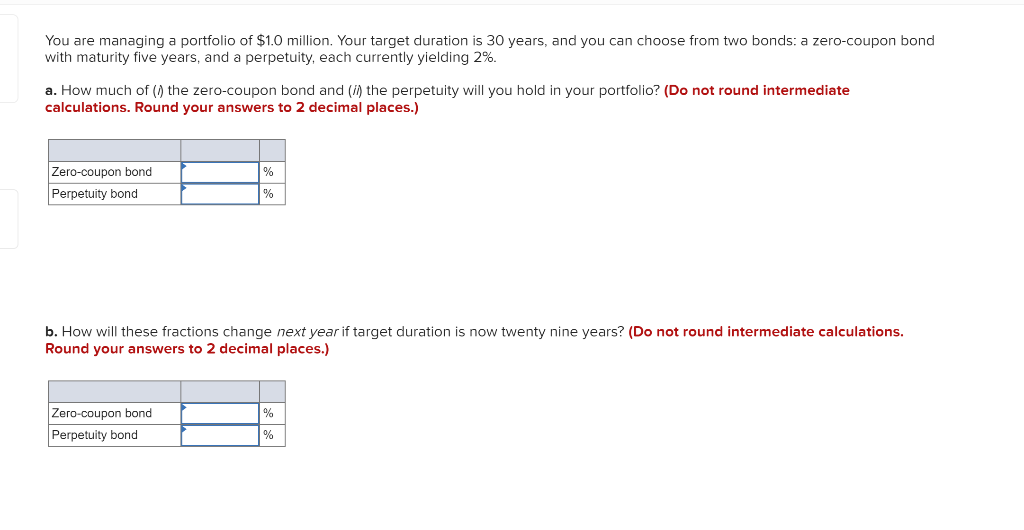

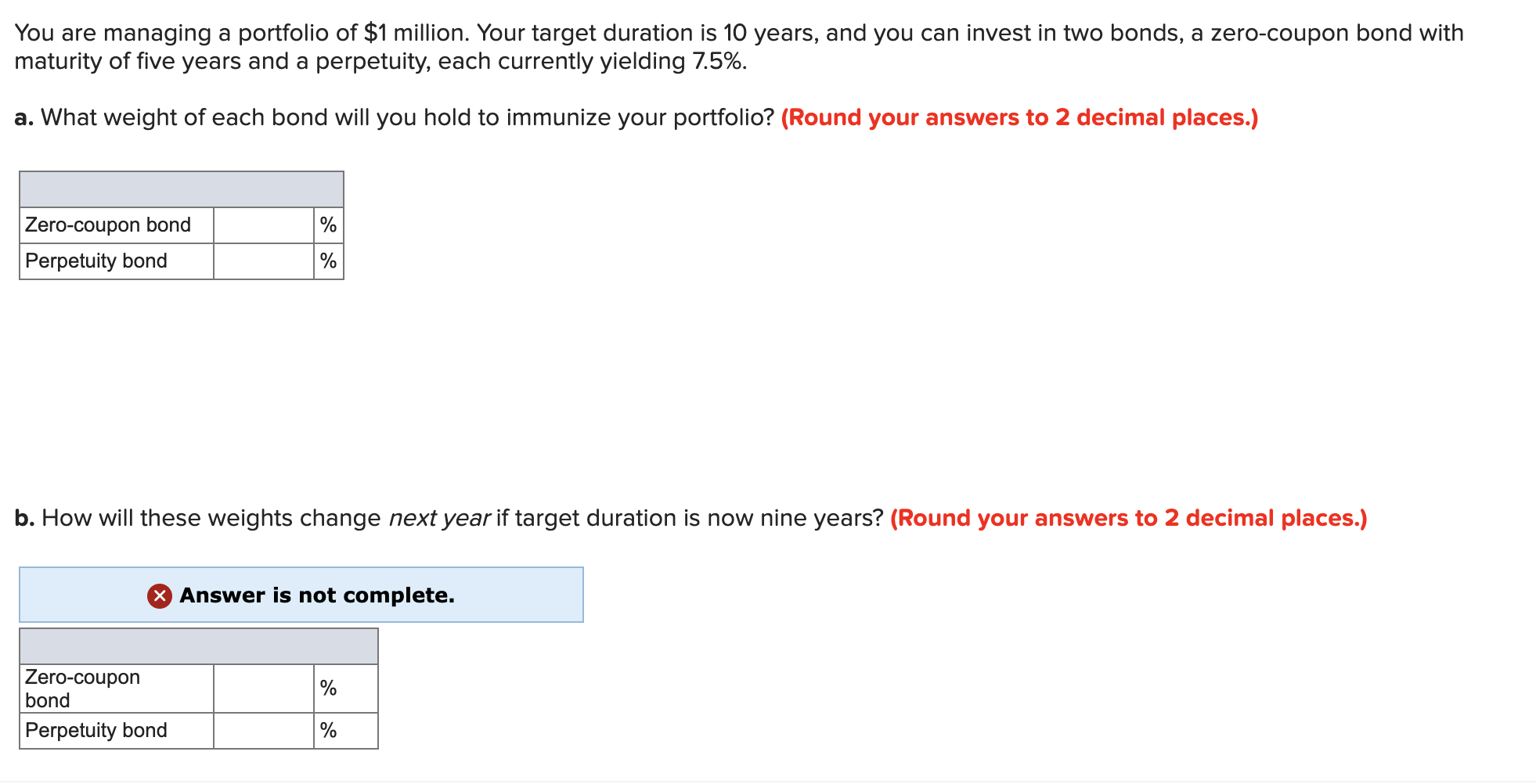

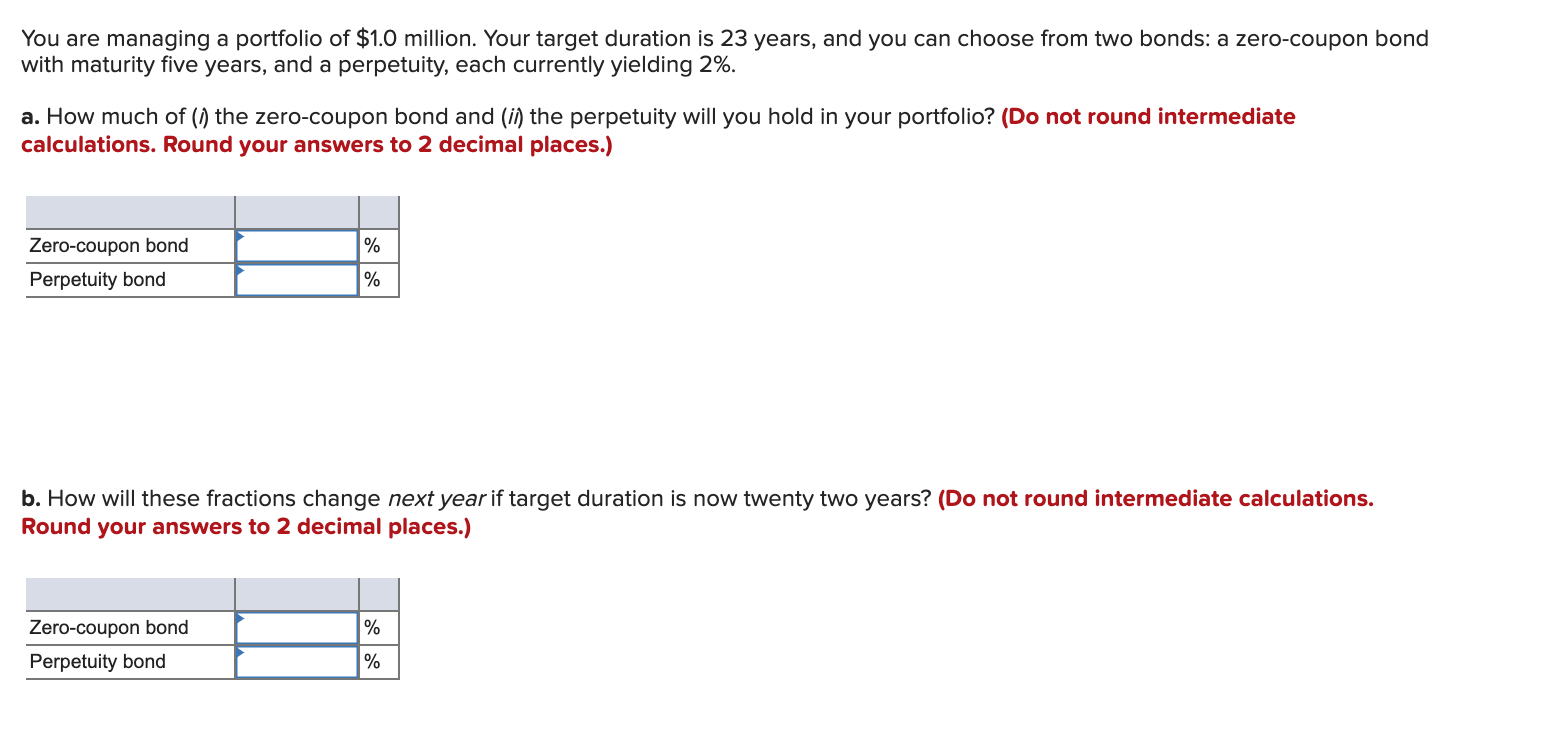

Solved You are managing a portfolio of $1.0 million. Your ...

PPT - 8. Measuring Interest Rate Risk-- Duration and ...

Zero-Coupon Bond Definition & Meaning in Stock Market with ...

Problems 63–66 involve zero-coupon bonds. A zero-coupon bond is a bond that is sold now at a discount and will pay its face value at the time when it matures; no interest payments are made. ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

Duration and Convexity in Bond market

SOLVED:Unvolve zero-coupon bonds. A zero-coupon bond is a ...

Solved a). What is the 1-year, 2-year, and 3-year spot ...

Chapter 4 Bond Price Volatility Chapter Pages 58-85, ppt download

Duration and Convexity, with Illustrations and Formulas

Zero Coupon Bond Introduction · Fixed Income

Investment Improvement: Adding Duration to the Toolbox | St ...

Bond duration - Wikipedia

Solved You are managing a portfolio of $1 million. Your ...

Solved You are managing a portfolio of $1.0 million. Your ...

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

Modified duration of zero-coupond bond (FRM practice question)

Reserve Bank of India - Database

Under the Hood: What You Need to Know About Bond Duration and ...

Yields & Prices: Continued - ppt video online download

Convexity of a Bond | Formula | Duration | Calculation

Consider a zero coupon bond with face value F, | Chegg.com

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Investor's Guide to Zero-Coupon Municipal Bonds | Project ...

WWWFinance - Bond Valuation: Campbell R. Harvey

![PDF] Duration and convexity of zero-coupon convertible bonds ...](https://d3i71xaburhd42.cloudfront.net/39b5487ce4f8becdfb0faf5ae6e30fd10537436c/13-Figure5-1.png)

PDF] Duration and convexity of zero-coupon convertible bonds ...

Finding YTM of a Zero Coupon Bond (6.2.1)

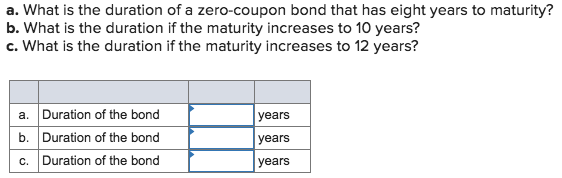

Macaulay Duration

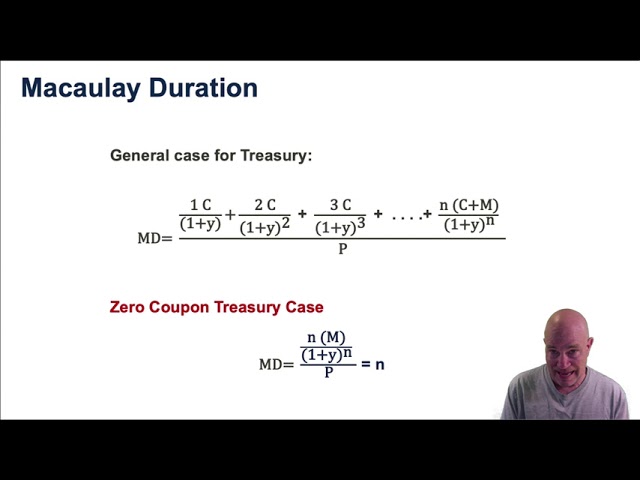

Solved a. What is the duration of a zero-coupon bond that ...

Zero Coupon Bond Value - Formula (with Calculator)

Advanced Bond Concepts: Duration | The Financial Engineer

The Key To Duration: Sensitivity To Changing Interest Rates ...

Macaulay Duration

Duration and Zero Coupon Bonds - YouTube

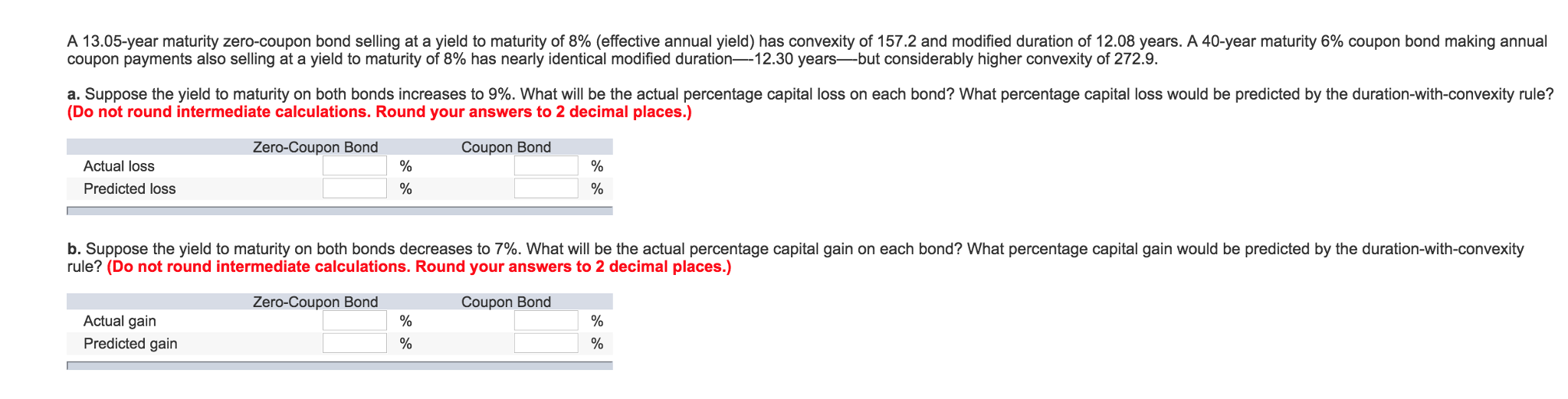

Solved A 13.05-year maturity zero-coupon bond selling at a ...

When do key rate measures add up? - Scanrate

Actuarial Exam 2/FM Prep: Find Term Structure for Zero Coupon Bonds Given "Ordinary" Bond Info

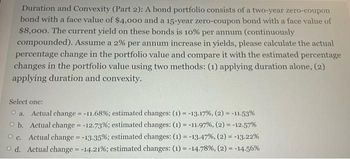

Answered: Duration and Convexity (Part 2): A bond… | bartleby

Bonds of Mass Destruction - The Last Bear Standing

Aha! Interest rates do matter.

Post a Comment for "43 duration for zero coupon bond"